Payroll Deductions

Implementing a workplace retirement plan may require you to adjust the way you administer your payroll for RRSP and TFSA employee deductions and RRSP, TFSA and DPSP employer contributions.

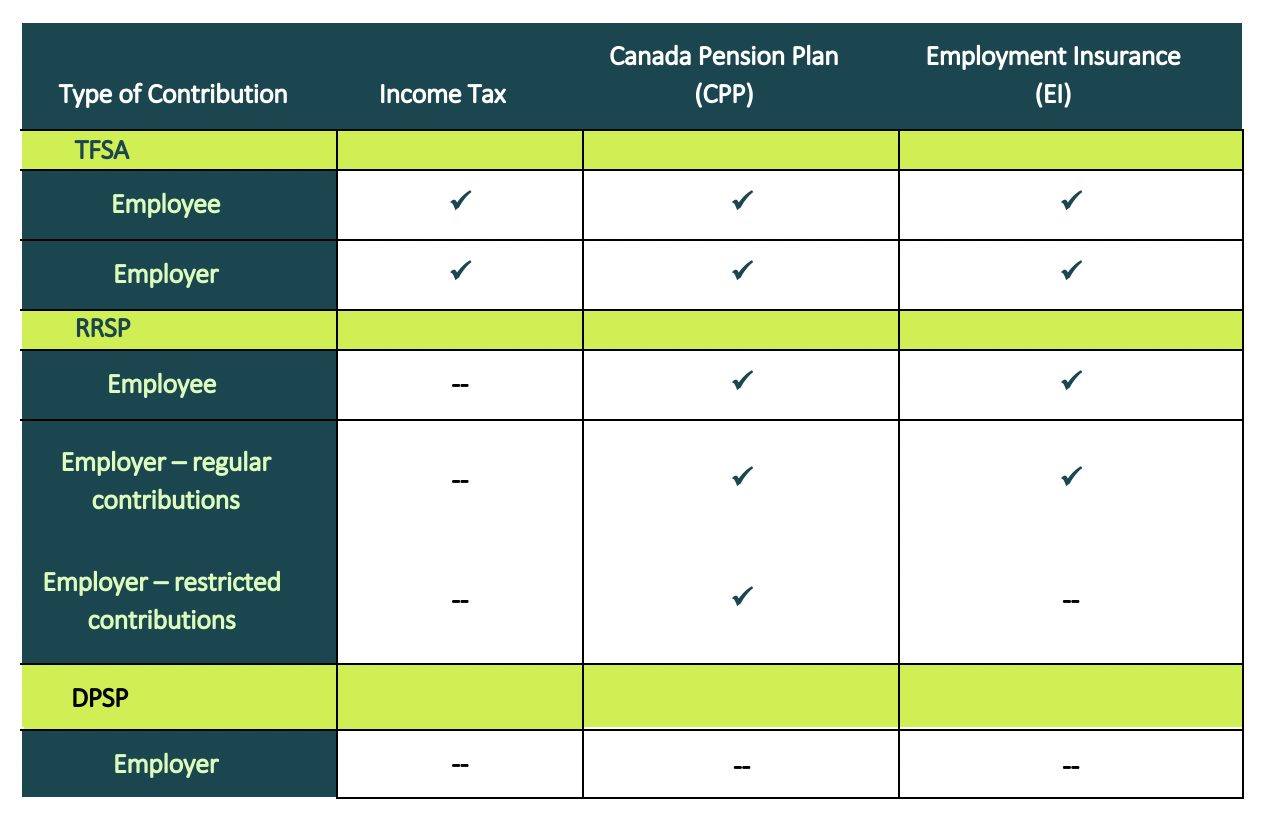

This chart provides a quick reference for when to include employee and employer contributions when applying payroll deductions (i.e., Income Tax, CPP, EI).

TFSA

Employee

- TFSA contributions are made after tax

- TFSA contributions require no special treatment for payroll purposes – deduct as you normally would

Employer

- Contributions are a taxable benefit if you are matching the employee contributions

- Include the amount of employer TFSA contributions as additional employment income for deductions:

- Canada Pension Plan (CPP)

- Employment Insurance (EI)

- Income Tax

- Include the employer TFSA contribution amount in Box 40 (Taxable Benefits) on T4 slips

TFSA EXAMPLE

Alex’s income is $4,000 monthly, and they are contributing 3% to the TFSA. The employer will match this with an equal amount (3%).

For payroll purposes:

- The employer TFSA contribution of $120 (3% of $4,000) is added to Alex’s employment income (to make it $4,120) to calculate the Income Tax, CPP and EI

- The employee TFSA contribution of $120 (3% of $4,000) is deducted from Alex’s pay after the deductions are calculated

- The employee and employer contributions of $240 is remitted to the plan

RRSP

Employee

- RRSP contributions are made before tax

- Do not deduct Income Tax from the Employee RRSP contribution amount made by payroll deduction

- Employee RRSP contributions do not affect CPP or EI deductions

- Deduct the amount of Employee RRSP contribution made by payroll deduction from income, to determine the amount of income tax to withhold

Employer

- Employer contributions are a taxable benefit if you are matching the employee contributions

- Include the amount of employer RRSP contributions as additional employment income for deductions:

- Canada Pension Plan (CPP)

- Employment Insurance (EI)

- If employer contributions to an RRSP are restricted, do not apply EI payroll deductions

- If you have reasonable grounds to assume the employee will be able to deduct the matching Employer RRSP contribution, then do not deduct Income Tax from the Employer RRSP contribution amount

- Include the employer RRSP contribution amount in Box 40 (Taxable Benefits) on T4 slips

RRSP EXAMPLE

Charlie’s income is $6,000 monthly, and they are contributing 5% to the RRSP. The employer will match this with an equal amount (5%).

For payroll purposes:

- The employer RRSP contribution of $300 (5% of $6,000) is added to Charlie’s employment income (to make it $6,300) to calculate the CPP and EI deductions

- The combined employee and employer RRSP contributions of $600 is deducted from Charlie’s employment income before calculating the Income Tax to withhold

- The employee and employer contributions of $600 is remitted to the plan

RRSP/DPSP

Employee

- RRSP contributions are made before tax

- Do not include employee contributions as a taxable benefit when calculating the amount of income tax to deduct

- Employee RRSP contributions do no affect CPP or EI deductions

Employer

- DPSP: Employer contributions are not a taxable benefit and are not tax deductible by the employee

- RRSP: Employer contributions are a taxable benefit and are tax deductible if you are matching the employee contributions

-

Do not include the amount of employer DPSP contributions as additional employment income for deductions to:

- Canada Pension Plan (CPP)

- Employment Insurance (EI)

-

Report a Pension Adjustment (PA) for annual employer contributions made to the DPSP on behalf of an employee. Show the amount in Box 52 (Pension Adjustment) on T4 slips

- A PA will reduce the employee's RRSP contribution room in the following year

RRSP/DPSP EXAMPLE

Charlie’s income is $6,000 monthly, and they are contributing 5% to the RRSP. The employer will match this with an equal DPSP amount (5%).

For payroll purposes:

- The employer DPSP contribution of $300 (5% of $6,000) is not added to Charlie’s employment income to calculate the CPP and EI

- Only the employee RRSP contribution of $300 is deducted from Charlie's employment income before calculating the Income Tax to deduct

- The employee RRSP and employer DPSP contributions of $600 is remitted to the plan